The AI revolution is often compared to past technological waves, from the spread of electricity to the rise of the internet. Each of these transformations followed an S-curve pattern of adoption: slow at the start, then rapid acceleration once infrastructure matured and costs fell, and finally saturation when nearly every household, enterprise, and institution had integrated the technology. Looking at the current trajectory of AI, the evidence suggests we are only in the very beginning of this cycle—closer to the mid-1990s internet era than the 2010s smartphone boom.

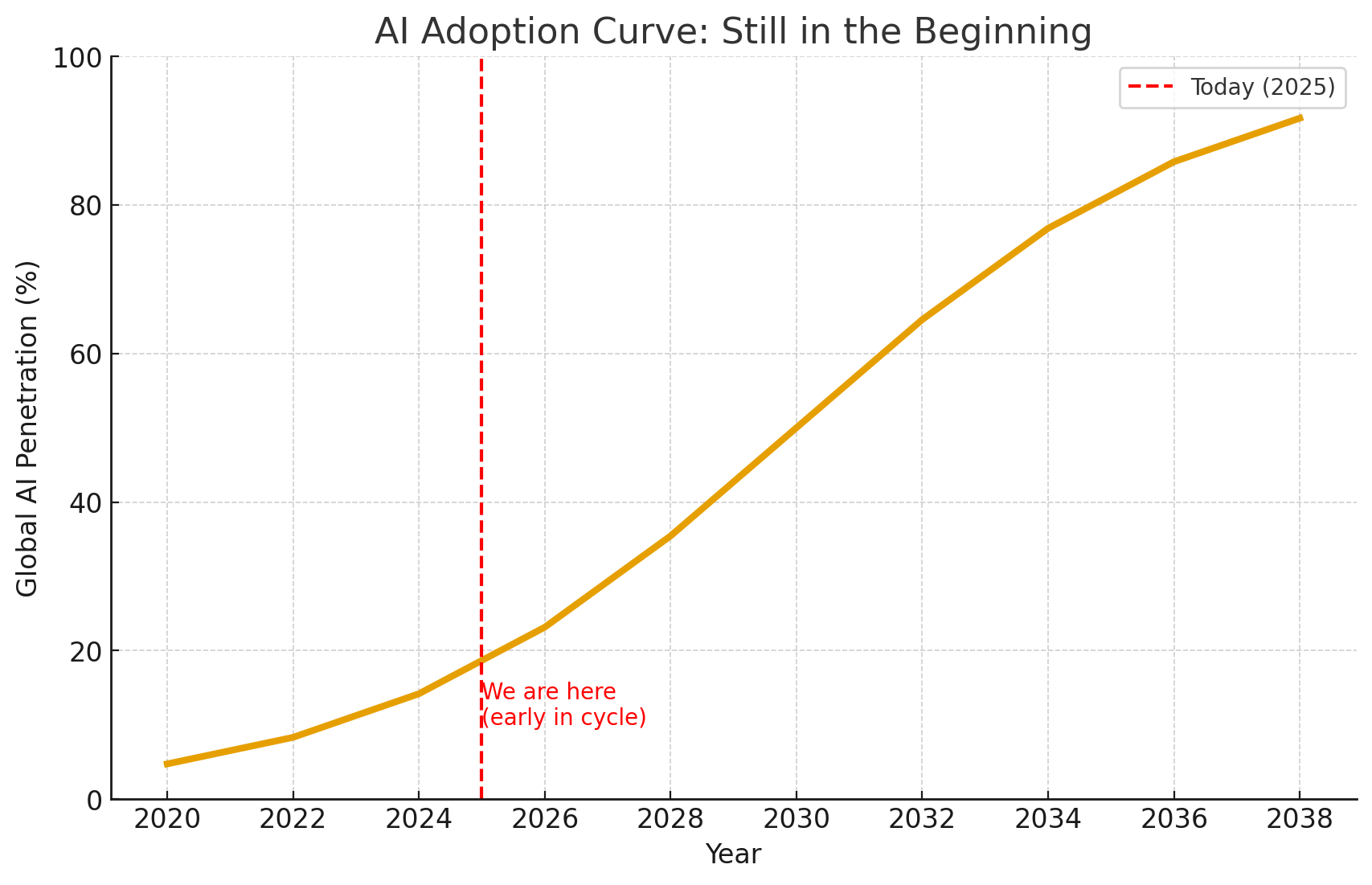

The adoption curve visualization highlights this point. Today, in 2025, penetration remains in the early phase of the S-curve. While headlines are filled with record data center spending, AI chip shortages, and sky-high valuations, the actual deployment of AI across enterprises and consumers is still relatively modest. A majority of companies are testing AI copilots or experimenting with generative tools, but very few have embedded them at scale into mission-critical workflows. Similarly, consumer usage of AI is more experimental than systemic—millions of people have tried chatbots, but few rely on them daily the way they do email or mobile banking.

The implication is that the acceleration stage, where adoption curves bend sharply upward, is still ahead of us. Over the next decade, we are likely to see AI transition from pilot programs into standard operating infrastructure, powering everything from customer service and logistics optimization to healthcare diagnostics and national defense. This acceleration will coincide with broader infrastructure improvements: greater availability of GPUs and custom inference chips, expansion of grid capacity to power AI factories, and regulatory frameworks that build trust in responsible deployment. Once these conditions align, AI penetration could surge rapidly—echoing the internet’s climb from niche academic tool to universal business necessity within a decade.

For investors, this perspective carries significant weight. If AI is only in its first third of adoption, current valuations may represent less a speculative bubble and more the premium investors are willing to pay for early access to exponential growth. Leaders in compute (Nvidia, AMD, Broadcom), hyperscale infrastructure (Microsoft, Amazon, Google), and applied AI platforms are positioned to capture disproportionate value as adoption accelerates. Conversely, the risk lies not in overestimating the hype, but in underestimating how quickly AI can become indispensable once its cost curves and use cases reach scale.

The adoption curve reminds us of a simple but powerful truth: today’s AI excitement is not the end of the story, but the beginning. The steepest part of the curve still lies ahead, and with it, the compounding effects that will shape economies, companies, and societies for decades to come.